The Zero-Down Wealth Strategy: Why Smart Canadians Are Getting Positioned Now

Why Smart Canadians Are Getting Positioned Now

By Erwin Szeto | Host of The Truth About Real Estate Investing for Canadians

Recorded: April 2026

Host: Erwin Szeto, The Truth About Real Estate Investing for Canadians Podcast

I’ve been doing this podcast since 2016. Almost 10 years, approaching 500 episodes. And in all that time, I’ve rarely recorded a solo episode — because this strategy is so important, and so few people are talking about it, that I needed to speak directly to you, my precious 17 listeners.

I call it the Zero-Down Wealth Strategy. And if you’re a Canadian real estate investor who’s tired of tenant headaches, over-concentrated in local real estate, and wondering what comes next — this might be the most important thing you read this year.

The $433 Question

Let me ask you something.

Would you rather invest $100,000 — or $433 a month?

Most people hear $100,000 and immediately think: I don’t have that sitting around. But $433 a month? That’s a car payment. Most of us spend or invest that without blinking.

Here’s the thing — they’re the same investment.

$433 is the monthly interest cost of a $100,000 investment loan (from an institutional lender — none of that private lending crap) at today’s rate of 5.2%. One credit check. One self-reported loan application. Zero of your own capital required. No property or property appraisal. No lender fees, mortgage broker and full underwriting.

That’s it.

Why Canadian Real Estate Investors Are Stuck

Before I explain the strategy, I want to acknowledge something most of us feel but rarely say out loud.

We’re stuck.

Inflation is real. In March 2026, Canada’s inflation rate hit 3.3% — well above the Bank of Canada’s 2% target. Just look at what it cost to build the Eglinton LRT if you want a concrete example. Money sitting idle loses real purchasing power every single month.

We’re over-concentrated. Almost every real estate investor I meet with to discuss their investments has 80 to 90% of their wealth tied up in local Canadian real estate — all in Canadian currency. That’s not diversification. That’s concentration risk.

Demand is weakening. Immigration restrictions, rising unemployment, softening rental demand — the outlook for Canadian investment property has changed materially. This is not 2015.

The landlord nightmare is real. I say this as someone who’s lived it. I had a tenant deliberately flood my basement causing $10,000 worth of damage. The police couldn’t do anything. I’m currently nine months into a Landlord Tenant Board hearing just for non-payment of rent. Non-payment. Vandalism. LTB backlogs. Ontario is one of the most difficult places in the world to be a landlord right now.

So why are we still playing the same game?

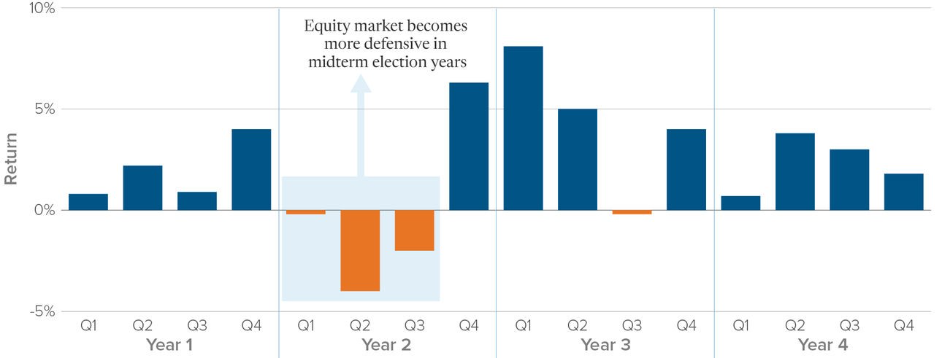

2026: A Critical Window

Here’s what makes this moment particularly important.

2026 is a US midterm election year — and history has a very clear pattern:

- 4.7% — Average S&P 500 return in midterm election years (vs. 9.5% in all other years)

- 18% — Average intra-year market drawdown before the November election

- 15.4% — Average S&P 500 return in the year after a midterm election

Quarterly average S&P 500 price returns by presidential cycle (1961-2024)

Source: Strategas Research

We are in Q2 of Year 2 RIGHT NOW and this year should be especially volatile with this November’s midterm election deciding if Trump controls Congress or not.

The market already dropped 9% earlier this year and bounced back 12% — exactly the kind of volatility midterm years are known for.

The dip before November isn’t the danger. It’s the setup.

The question isn’t whether a correction is coming. The question is whether you’ll be positioned to benefit from the rebound when it does.

You Already Believe in Leverage

If you’re a real estate investor, you already understand this concept — you’ve just been applying it to the wrong vehicle.

Nobody buys investment property with cash. We put 20 to 25% down and borrow the rest. We call that smart investing.

Around 2010 — right after the financial crisis — zero down and 5% down mortgages were everywhere in the investor community. Nobody called that reckless. We called it getting ahead. And everyone I know who took advantage of that leverage in 2010 did extremely well.

This is the same principle. Just applied to a better vehicle — one with no landlord headaches, no appraisals, no LTB hearings, and no midnight calls.

Two Yale Professors Proved It

In 2010 — right after one of the worst decades in stock market history — two Yale professors published a book called:

Lifecycle Investing: A New, Safe, and Audacious Way to Improve the Performance of Your Retirement Portfolio

— Barry Nalebuff & Ian Ayres, Yale University

Their conclusion, backed by rigorous mathematical proof: leveraged investing, done correctly, outperforms conventional portfolios over a lifetime.

They weren’t writing from the comfort of a bull market. They ran the math through the pain — through the dot-com crash, through 2008 — and the conclusion was the same every time.

We real estate investors already know this intuitively. We leveraged into real estate and built wealth over the long term. This is no different in principle. It’s just a different asset class.

The Stress Test Results

I ran my own stress test — comparing a leveraged non-registered investment against three alternatives most Canadians swear by:

| Strategy | Result |

| RRSP — pre-tax dollars, tax-deferred growth | ✗ Underperforms |

| TFSA — after-tax dollars, tax-free growth | ✗ Underperforms |

| Non-registered, unleveraged | ✗ Underperforms |

| Non-registered, leveraged | ✅ Wins |

Yes — including the TFSA. The leveraged non-registered strategy beats them all.

I know that’s counterintuitive. We’ve been conditioned to think TFSAs and RRSPs are the gold standard. And for most people, they are excellent choices. But real estate investors aren’t most people. We walk to a different drummer. We’re looking for outsized returns — and the math confirms this strategy delivers them.

You can verify this yourself — run the numbers in ChatGPT or Claude and it will confirm: a non-registered leveraged investment outperforms registered fund vehicles over the long term.

How It Actually Works

Here’s the practical breakdown:

Step 1 — Qualify One credit check. One self-reported loan application. No property, appraisal, mortgage broker and no full underwriting involved.

Step 2 — Borrow $100,000 100% loan to value. Zero of your own capital required. Your only cost is $433/month in interest at 5.2%. If structured correctly, that interest is tax-deductible — speak to your accountant.

Step 3 — Invest The $100,000 goes into a segregated fund account — think of it as a mutual fund from the insurance industry.

Step 4 — Principal protection This is the key difference from simply putting borrowed money into the stock market. Segregated funds come with built-in principal protection. The downside is covered. The upside belongs to you. That’s why institutional lenders are willing to lend against this — the risk is contained.

The accounts belong to you. You sign off on everything. We coordinate the paperwork and movement of funds at iWIN Wealth Planning — but it’s your money, your account, your decision.

Is This Right for You?

Leveraged investing isn’t for everyone. Before you consider this strategy, ask yourself these questions — and discuss them honestly with your advisor.

Do you have a specific financial goal in mind?

This strategy works best when you know what you’re building toward. Retirement income? Diversification away from Canadian real estate? Getting off the landlord treadmill? Get clear on your goal before you start.

How long are you planning to invest?

Leveraged investing is typically more suitable for a long-term investment horizon of 10 years or more. Just like real estate — the longer you hold, the more you de-risk. This is not a short-term play.

How much other debt are you carrying?

Keep your debt manageable. Make sure your current debt load is under control before adding an investment loan. A good rule of thumb: your total monthly borrowing costs — including the $433/month investment loan interest — should not exceed 36% of your before-tax income.

How stable is your income?

A steady income helps you make the required interest payments every month without stress. If your income is unpredictable, this may not be the right time.

What is your tolerance for risk?

Are you comfortable with potential fluctuations in your investment value? And with the possibility that in some scenarios, leveraged investing may not outperform traditional investing? If market volatility keeps you up at night, this is not the right vehicle for you.

Let’s talk if you answered these questions honestly and still feel confident

If I Could Do It All Again

I want to be honest with you.

I made the decision in 2005 — 11 years before this podcast started — to go all-in on real estate investing instead of the stock market. And I’ve built a great business from it. Nearly $500 million in investment property transactions. Four-time Realtor of the Year to investors in Ontario.

But if I could do it all again? I would have deployed leverage earlier — into vehicles without the landlord baggage.

Less grey hair. More money. No tenant nightmares. More time with our families.

I think about my clients too. The ones I’ve worked with for years. We would have all made more money. We would have all been happier. That’s not a small thing.

These are the same strategies I’m now teaching my own kids — and recommending to every client I meet. Because I don’t want non-payment of rent or tenant vandalism stealing anyone’s time away from what actually matters. My future grandchildren deserve parents who aren’t fighting about money because they have to feed the real estate’s bank account — because a tenant stopped paying or a basement flooded, which is happening ever more frequently with climate change.

The Midterms Are November. You Have 6 Months.

The US midterm elections are November 2026. History says markets dip before then — and then deliver some of the strongest returns of the four-year presidential cycle in the year that follows.

You have roughly six months to get positioned.

I’m doing a free live training where I walk through the full strategy, show you the stress test results side by side, and answer your questions directly.

Two ways to join:

📍 Saturday May 30, 2026 — Hybrid (In-Person + Zoom) Doors open 8:30am · Hard start 9:00am · Hard stop 10:30am · iWIN Office, Oakville · Limited to 40 in-person

[Register here → Wealth Planning for Canadians]

💻 Tuesday June 3, 2026 — Webinar Only 8:00pm Eastern · Zoom · 90 minutes

Same content both sessions. Pick what works for you.

[Register here → Wealth Planning for Canadians]

In-person spots fill fast. Don’t wait.

To Listen:

Audible: https://www.audible.ca/pd/B0GYYHMYXG?source_code=ASSGB149080119000H&share_location=pdp

Apple Music: https://podcasts.apple.com/ca/podcast/the-zero-down-wealth-strategy-how-canadians-use/id1100488294?i=1000764468055

YouTube: https://youtu.be/ibBWxozAre8

You’ve Built Wealth. Now It’s Time to Understand It.

You’ve Built Wealth. Now It’s Time to Understand It.

After dozens of consultations, I’ve noticed the same pattern again and again: most investors have built real wealth, but they’re not confident they can retire from it. They’re sitting on $2M–$5M in property but feel cash-flow poor. They’re paying more tax than they should because everything is held in personal names. They have no liquidity, no insurance strategy, and no clear plan for what happens if something happens to them. And almost every single client tells me the same thing: “I don’t actually know what retirement looks like for us.”

Real estate builds equity, but it doesn’t automatically build freedom. Without a coordinated plan for taxes, income, protection, and exit strategy, investors often end up working harder in retirement than they did in their 30s. That’s why I created the Wealth Freedom Blueprint – a simple, practical guide to help you understand where you stand today, what gaps are costing you money, and how to turn the wealth you’ve built into a life you can actually live.

Download your free Wealth Freedom Blueprint

Final Thoughts

Whether you’re building wealth, protecting it, or preparing to transition it, you deserve a clear, tax-smart strategy that works in real life.

That’s what iWIN Wealth Planning is here for.

This is how we’re creating predictable, stress-free wealth for Canadian families…

so you can enjoy the life you’re building.

Book your Wealth Planning Call

Sponsored by… Me!

This episode isn’t sponsored—except by my wife Cherry and me. Real estate investing is our life. It’s helped us build wealth and achieve peace of mind about retirement and our children’s future.

Till next time—just do it. I believe in you.

Erwin Szeto

W: erwinszeto.com

FB: facebook.com/erwin.szeto

IG: @erwinszeto

Disclaimer

As a committed advocate for transparent and responsible investing, I want to disclose that I am an Advisor to SHARE SFR (Single Family Rental). I hold equity in the company and earn referral commissions from clients I refer.

My endorsement of their model—focusing on positive cash flow and direct ownership—is based on personal experience and belief. Still, every investor should do their own due diligence.

Leave a Reply

Want to join the discussion?Feel free to contribute!